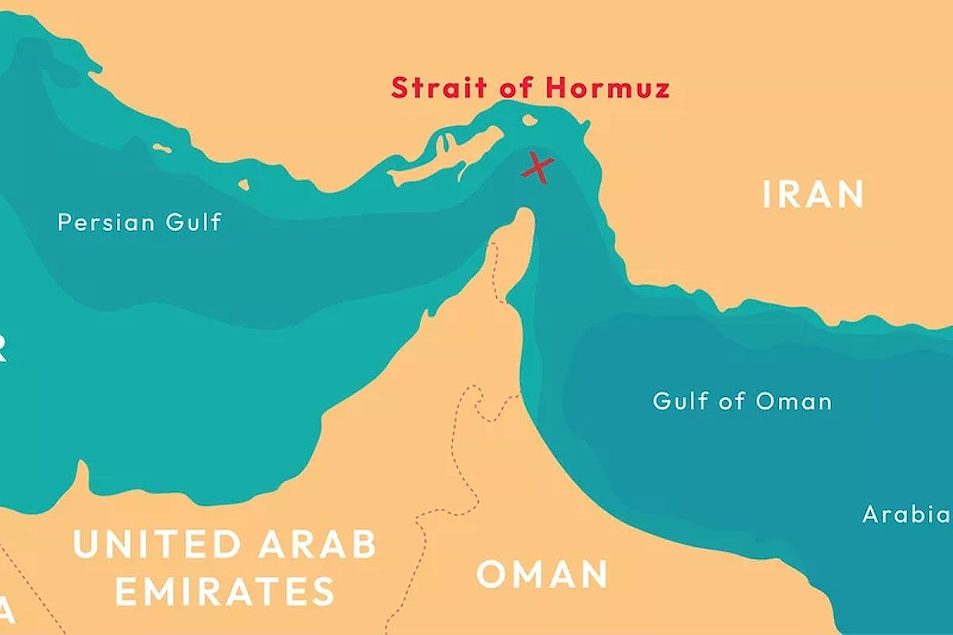

KANSAS CITY — Energy is the backbone that keeps all commodity markets flowing. Even a minor hiccup in supply or access can cause disruptions. The closure at the Strait of Hormuz, a vital channel that was funneling 20% of the global oil supply, has significantly impacted the flow of commodities worldwide.

Tim Statts, vice president of commodity services at Schneider Electric, where he leads a team responsible for analyzing energy commodity markets and developing comprehensive strategies for managing associated risks, provided some insights into the situation and its rippling impact. Statts plans to delve further into this topic and what it means for the commodity ingredients markets during his presentation at this year’s Sosland Purchasing Seminar event.

Milling & Baking News: The conflict with Iran and the closure at the Strait of Hormuz seem to have significantly impacted global energy markets. How much do these events weigh on the US market?

The oil market is a pretty globalized market. Whereas natural gas has some global elements to it that can cause prices to move some, they don’t fully align across the globe the way that crude oil prices do. So, if the Strait of Hormuz is blocked and 20% of the world’s oil comes through the Strait of Hormuz that means that it’s going to impact the global price of energy regardless of the U.S. being the number one oil producer. It’s going to have an impact because the oil moves in so many different directions for so many different reasons, so it impacts us all. We see it at the pump. But diesel is really getting hit hard because diesel is very restricted, and not being able to clear out the Strait is a big problem.

MBN: If the United States is a net exporter of energy, then why are US gas prices rising?

Tim Statts, vice president of commodity services at Schneider Electric.

| Photo: Schneider ElectricThe other thing that we are is the largest demander of oil. We’re just not the largest supplier; we’re also the largest demander of oil. And on top of that, there are different grades, different variations. We still import some, we still ship oil out, and so, again, it is a truly global market. Our production is probably about 13.5 million barrels, maybe 14, but we still demand 18 to 20. So, our demand is still higher than our supply. But what’s really happened is OPEC kept trying to restrict supply. And what they were hoping to do is push up prices, but what they found was that the U.S. could continue to supply more oil. And they thought the U.S. couldn’t do that. So what they realized was that the U.S. is going to likely continue to build more supply and bring more new supply online, so they decided to reverse this and put more oil into the market, so they were in the process of doing that. And their theory that they would slow down the U.S.’s ability to grow if they get to a certain pricing threshold, probably in the $50 to $60 (per barrel) range, but Hormuz happened and now they can’t move all their oil where they want to, and this supports us continuing to grow our oil. But again, we demand a lot. So maybe that demand will get cut back a little due to price response, but it won’t likely get cut back below what we produce. And we still import certain types of crude for the refineries that we have because they are different supplies. There’s sweet, there’s sour crude, there’s different types of crudes, and not every refiner can accept all the different types of crudes that are out there. So sometimes we will bring one type of crude in and ship one type of crude out, and that’s something that isn’t always understood by the general public. It’s often not understood by administrations, and that’s often why some people want to tap the reserves. Those are some of the reasons why we’re feeling an impact, but the biggest reason, I think, is that we are a big demander and people forget that. Even with us being the number one producer in the world, we don’t meet our internal needs.

MBN: Is the demand for oil still growing in the United States?

It typically is. One of the things that competes with that is this idea that we’re bringing more non-fossil fuel vehicles to bear. But the reality is we haven’t seen that grow to the level that’s just fully displaced and reduced oil demand. Not at this point. If you look at global crude demand, it is up quite a bit, but some of the US demand is starting to be flat and maybe grow less, at least in the upcoming year. But, I think that if you go out two or three years, we’ll start to see a little bit more growth than that. But part of that lack of growth is the factor of pricing. So, at a normal price, would we continue to grow? Yes. But at a price like $4 (per gallon), you do see some response. Whether it’s carpooling or driving to fewer places.

MBN: When the Strait reopens, how long will it take for energy markets to feel that effect?

When they reopen, OPEC is going to work hard, and they’re going to try to work fast to try to restore their output. And it probably takes about 4 to 6 weeks for that to come back online. Now beyond that, the OPEC again has been focused on increasing their output. They were in the process of trying to reduce the (global) supply, but what they found was the U.S. was able to keep producing, so they changed tactics and said they were going to put more production into the market in an attempt to reduce the U.S.’s market share. Once the Strait opens, I think we’ll ultimately go back to this status quo that was tracking toward OPEC finding a way to put more oil on the market in an attempt to push prices a little bit lower, what they would hope would be in the $50-range (per barrel) and try to reduce significantly the U.S.’s ability to drill new wells and bring new production online. Because the U.S. has hit all-time highs in production recently, and OPEC did not expect that. They thought the U.S. had kind of capped out, and so they thought if we lower our production, that will lower the world production, and it didn’t really happen that way. We filled the gap.

MBN: That’s an interesting strategy for OPEC. What’s the logic behind it?

They’re basically saying we’re going to reduce our revenue in the near term in an attempt to recoup more of our revenue by pushing the U.S. somewhat out of the market and not allow them to continue to build their market share. So, OPEC in general thinks long term. They’re not always right. They sometimes make mistakes, but they don’t always think in terms of what’s best for me next week or even what’s best for me next month. They think longer term whereas you could make the argument that the U.S. production largely just responds to pricing signals. If it’s $30 oil, they’re not going to drill a well because their breakeven costs are probably in the $50-range. Some of the places in OPEC, their breakeven costs are lower than that. A lot of the oil we’re drilling for is coming out of shale, and it’s just more expensive to get it. But (OPEC countries) have a lot, and they have pretty easy access to it. So, they’re still profitable at $50.

MBN: Have the recent events in Venezuela impacted the global supply situation, and will that eventually effect pricing?

Venezuela has a ton of reserves. When you think about Venezuela, it’s not so much that they have a ton of supply, it is much more that they have a tremendous amount of oil reserves. But they haven’t brought all that to bear, largely because, even now, there’s always conflict and battles about which companies are allowed to go in there and drill for the oil, so it’s not something that has any real impact on pricing. And I can’t speak to whether the (Trump) administration thought it would help, and maybe (President Trump) did that first before going to Iran or if they’re just completely separate events, but it doesn’t have much impact that I can see.

MBN: What else is driving the energy markets today?

From a crude side, you’re looking at a situation where you’ve got food prices jumping, and the Strait is a part of that. That is a real impact. For example, Saudi Arabia went from about 10.5 million barrels to about 8.5 million barrels (per day). They lost two million barrels because they can’t get it through the Strait. When you think about the Strait, you’ve got to think about it in terms of supply being curtailed. It is literally being taken offline to some degree. So, there’s stranded supply out there and the demand response is never that fast. If we cut off shipping 20% of the oil, the market knows it, but demand won’t respond as fast. Consumers don’t immediately say, “Oh, my gas price went from $2.80 to $4, I’m not leaving home now.” It takes some time. So, in my view, it is the biggest driver, and everything was bearish before because we had positive net change to storage, everything was moving along, things were fine. Then all of a sudden, the Gulf countries have to slice their drift and that is a big deal. So for me, that is the biggest driver. It has an impact on demand and so demand will respond to that and we’re starting to see some of that. But if you took that out, I think I would be going into this conference saying I think we’re a little bit oversupplied and prices are a little bit bearish. That’s where we would have been. From July to February, we had some sort of slight net positive change. Anywhere between a half million to 2 million barrels per day supply excess to demand. It was really a bearish situation.

#closure #Strait #Hormuz #impacting #energy