Khanchit Khirisutchalual/iStock via Getty Images

Performance Commentary

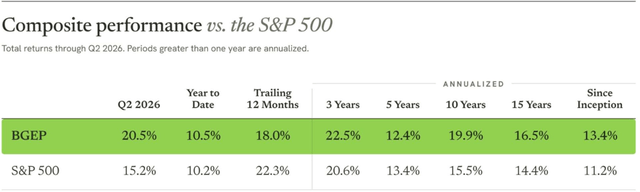

The second quarter was a strong bounce back from a difficult start to the year. Last quarter, we noted that markets have historically rebounded 70% of the time in the quarter immediately following a negative one, and this proved to be one of those instances. The portfolio returned 20.5% in Q2 versus 15.2% for the S&P 500, pushing our year-to-date return back ahead of the benchmark.

Fund Inception 8/18/05. Portfolio performance reflects Broadleaf’s Growth Equity Composite, described more fully under the caption “Performance Disclosures.” You are urged to read that information in its entirety in connection with any evaluation of Broadleaf’s performance statistics. All figures are shown net of actual fees. Any assumed fees have been calculated on a pro forma basis, reflecting the highest fee levels that Broadleaf would charge clients per our disclosures in Part II of our Form ADV.

Market Review and Outlook

There is certainly no shortage of topics to discuss, as it feels like 3 years of news has been fit into the last three months. Mega-IPOs, war, inflation, and most importantly AI all left an imprint on the quarterly tape.

A compromise to end the Iran War has been elusive, as Trump’s Art of the Deal struggles to gain traction in the world of geopolitics. While US foreign policy has long abided by the old adage that, “we do not negotiate with terrorists”, it seems like the current administration is quite eager to make a deal with Iran. Absurdly, we have noticed that re-escalation typically occurs between the hours of 4 PM on Friday and ends by 9:30 AM on Monday. Due to our day jobs, we thank the President for that, but frankly we aren’t quite sure what to make of the Strait of Hormuz drama.

Partially as a result of the higher energy prices brought on by the war, the consumer has dealt with rising inflation and a Fed unwilling to cut. The result is a depressed but stable consumer. Not bad, but given the broader landscape, perhaps uninspiring from a growth investing standpoint.

In the absence of the current technology capex boom, the economy would likely be languishing along, perhaps marred still by a post-pandemic hangover and high prices. Many consumer goods companies have been forced to lower prices after years of aggressive price increases (goodbye $7 Doritos). While the broader consumer economy might be best described as “just okay”, the AI boom is responsible for over half of the 2.1% GDP growth seen this quarter. From this lens, growth investors seem to be justified in focusing their investment opportunities into AI. In other words, it is important to keep the biggest thing front and center.

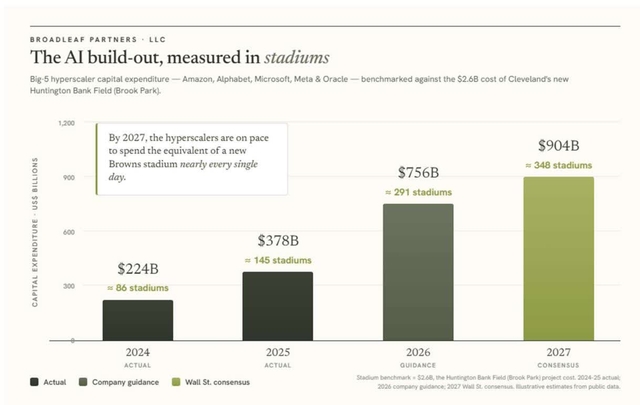

In an attempt to quantify the amount of money being spent on AI datacenters, Doug and I like to talk about AI in terms of the number of Cleveland Browns stadiums being built. I believe that this is Broadleaf’s first proprietary data set, and we are quite proud of it, mostly because we are long-suffering fans, but also because we think it illustrates just how large this buildout is. Perhaps next quarter we will quantify the boom in terms of Myles Garrett contracts, but for now we are still much too sad about that trade.

As you can imagine, trying to build a Browns stadium every single day is tough to do, and we question whether it can be done as fast as the money is being committed. The explosion of demand for data centers has led to acute shortages, giving the suppliers to data centers, the “bottleneck” companies, a massive amount of pricing power. Counterintuitively, these shortages are also elongating the cycle, giving the bottleneck companies a more predictable earnings stream in the intermediate future. Perhaps the most important bottlenecks are the formerly beleaguered memory companies, which are signing new customer commitments through 2030, highlighting the idea of a more durable cycle.

Investors have recognized the idea of bottleneck investing and have been following the cash flow cookie crumbs, leading to Wall Street’s newest moniker: “HALO” – Heavy Assets, Low Obsolescence. This boom is no longer just Nvidia, but also the entire semiconductor value chain. Also seeing a re-rating are energy/power generation, earthmoving equipment, and countless other tech hardware and heavy industrial plays. Following these cash flows has led to a rotation out of the spenders of capex (Mag7) and into the beneficiaries of this cash spend.

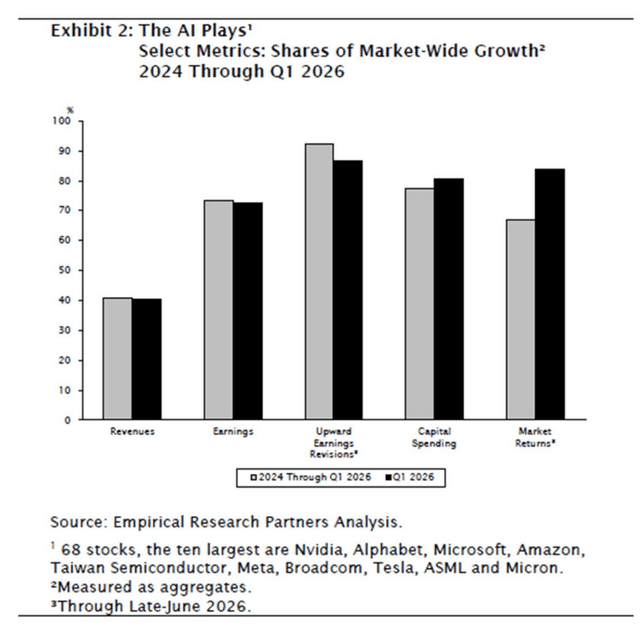

In an attempt to further quantify the market this quarter, the “AI Plays” account for well over 80% of this year’s market returns, a continuation from the first quarter. We have seen a variety of different attempts to quantify the impact of AI on the economy, but the chart below from Empirical Research Partners also paints the picture of an economy with a singular theme.

Exhibit 2: The AI Plays 1Select Metrics: Shares of Market-Wide Growth 22024 Through Q1 2026

Exacerbating this issue from the perspective of growth investing has been the potential disruption of the former darling software/SaaS business models by Artificial Intelligence. While it is too early to tell whether software is a dying industry, in experimenting with many of these models ourselves, it is hard to deny that this technology will change the business world forever. As a result of this market rotation, we cannot remember a time in which the dispersion of returns across growth investments has been higher.

This phenomenon does not end in the USA, as international markets have increasingly been driven by how much AI/tech exposure is embedded within their markets. On a global scale, semiconductors, hardware, and electronic equipment have sourced 70% of global stock market gains. Ranking returns by country is essentially an exercise in AI exposure, with countries like Korea and Taiwan seeing the greatest gains year to date.

One of our founding principles at Broadleaf is the three cycles of value. We acknowledge that economic cycles do and will change over time, perhaps in response to changes in supply/demand for certain goods and services (as we saw during the pandemic), but most convincingly to shifts in technology. As cycles shift, there are times to become more or less concentrated, depending on both our conviction as well as the relative opportunities presented in the market. This feels like one of those times, with the convergence of the economic and innovation cycles being a powerful combination for concentrated growth investing.

As it stands, our current and best thinking leans towards the idea that we are in the middle of a fundamental economic cycle regime change. Recent market moves hint at a future in which “HALO” assets are not just cyclical, but drivers of secular growth. The previous regime was driven by a digitally enabled consumer, highlighted by slow and steady growth, low inflation and the SaaS subscription. The current economic regime seems likely to be an enterprise productivity boom characterized by higher growth, higher inflation, and hard industrial assets. Our portfolio changes this quarter reflect our increased conviction in a new vision of the future.

While we are quite optimistic, we continue to monitor the AI boom for the following three main risks:

1. The Pace of AI innovation

2. AI Return on Investment

3. Political pushback to datacenters

We believe that there was relatively strong new evidence for model innovation and AI ROI this quarter, highlighted by the newest models released by Anthropic. Datacenters are likely to be on the ballot this November, especially here in Ohio, one of the datacenter hubs of the USA. We continue to monitor for signals of a productivity boom, and while it is not showing up in the data yet, we think this will come sooner rather than later.

While the societal impacts of technology are more debatable, the potential for economic progress is almost assured, as are the possibilities for things we can’t foresee. We remain incredibly optimistic about the future, and think that the second half of 2026 should be a positive one for growth investors.

About the Author

Pete is an Associate Portfolio Manager at Broadleaf, with a strong background in the financial services industry. He joined the firm in 2021, and has a proven track record of analyzing portfolio companies and identifying growth opportunities. Pete is a CPA and received his Chartered Financial Analyst (CFA®) designation in 2024. Pete lives in Hudson, Ohio with his wife Nicole and daughter Maisie.

Portfolio Characteristics

Investment Style

The Broadleaf Growth Equity Portfolio employs a concentrated growth style of investing, holding approximately 25-35 equity positions from a cross section of economic sectors. Morningstar would classify us as a large cap growth manager, but we will invest in select small and midsize companies as unique opportunities avail themselves. Sector exposures are strongly influenced by our views on three determinants of investment value, which we define as the economic cycle, the innovation cycle, and the credit cycle. Individual securities are ultimately selected on the basis of their long-term growth potential, profitability, and intrinsic value as measured by their free cash flow generating characteristics. Innovative ideas and themes are of particular interest.

Investment Objective

The portfolio’s goal is to provide equity-like returns and to outperform the S&P 500 over a three to five-year time horizon or full market cycle, utilizing a growth-oriented investment style. The portfolio is suitable for investors seeking exposure to a concentrated investment style which may be more volatile than the market as a whole. Investors should consider it as a portion of their investment portfolio within the context of their overall asset allocation and related investment goals.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

#Broadleaf #Partners #Growth #Equity #Portfolio #Review