Erik Isakson/DigitalVision via Getty Images

As value investors, we are always willing to take a look at companies getting beaten up by the market. After surging to $27 shortly after its IPO, we believed Fermi was substantially overvalued. Specifically, we noted that the actual cash raised over Fermi’s lifetime was a mere fraction of the market cap.

Fermi swiftly sold off.

It dropped another leg lower as news came out that its primary initial tenant had backed off a bit as described in the 10-K:

“The First Tenant LOI contemplated a phased deployment structure and included an exclusivity period that expired at midnight on December 9, 2025. Following the expiration of the exclusivity period, on December 11, 2025, the First Tenant notified us that it was terminating the AIAC”

This was particularly painful as it was Fermi’s only major LOI.

Finally, Fermi dropped another 18% intraday as its CEO left.

Fermi is now down 80% from its pricing shortly after the IPO. Perhaps now it is finally cheap enough to be worth buying. This article will examine Fermi at its new valuation and new fundamental situation.

Fermi is still not worth buying

At its reduced price, Fermi has a market cap of just over $3B. To be a good investment it has to be worth at least that much. Company value can come from 3 sources:

- Assets

- Operating business

- Proprietary ideas, people, and/or IP

We shall examine each category to estimate the fundamental value of Fermi.

Asset value

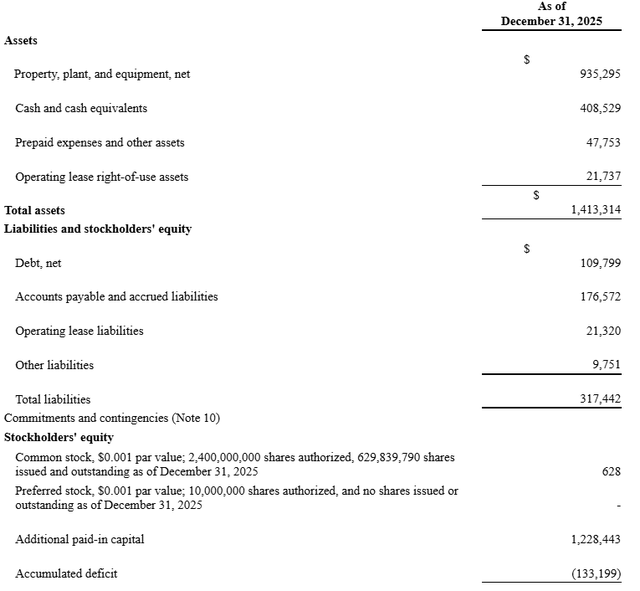

Fermi’s main assets are a land lease, some electricity generating equipment (recently ordered) and cash remaining from the IPO. As the assets were recently purchased, I would value them at the purchase price which is essentially the book value of assets listed in the 10-K. There has not been enough time for significant depreciation.

10-K

So that is asset value of $1.413B minus $317 million or roughly $1.1B of asset value.

Operating business

As a startup, Fermi does not yet have a real operating business. Per the 10-K, they have yet to generate revenue.

“We were formed in January 2025 and, as a development-stage company, have not generated revenue to date.”

They also do not have in-place future revenue as their initial tenant backed out.

With no current revenue and no in-place future revenue, it is hard to ascribe value to the operating business.

Thus, the value of Fermi rests in the intangible aspects. Some combination of ideas, IP, and people.

Fermi’s Idea Value

I think Fermi was initially trading on the value of its idea. It never had substantial assets or operations so its initially huge market cap was very likely due to the market being excited about Fermi’s core idea:

A mega-campus of self-powered data centers. Fermi’s 10-K describes the vision as consisting of 5 phases (0-4):

- Phase 0 – Site Enablement and Infrastructure Readiness

- Phase 1 – Initial Energization and Campus Activation

- Phase 2- Scaled Natural Gas Buildout and Combined Cycle Expansion

- Phase 3 – Construction of the First Nuclear Reactor and Continued Buildout of Gas Generation Capabilities

- Phase 4 – Expansion of Infrastructure and Construction of Additional Nuclear Reactors

They have largely completed phase 0. Future phases require significantly more capital some of which they have financed through the purchase of key electrical equipment. The full buildout of data centers, however, requires far more capital than Fermi has so it will require having actual counterparties with signed contracts such that it can be borrowed against.

Since the initial LOI fell through, revenue has been significantly delayed. It was initially scheduled to happen in 2026, but has been pushed to 2027. The 10-K details the change in calendar:

“Our initial development plan contemplated achieving approximately 1.1 GW of power capacity online by the end of 2026 through a combination of grid-supplied power, mobile generation, battery storage systems, and owned natural gas-fired combined cycle assets [ ] We continue to expect to achieve our longer-term objective of reaching approximately 2.0 GW of gas-fired and grid-supplied power online by the end of 2027, subject to completion of installation, commissioning, securing project financing, and tenant readiness milestones.”

I think the market correctly deduced that Fermi’s idea value was reduced with the loss of the LOI.

At least Fermi still had its people … until now.

When a company is in such an early startup phase, it really helps to be driven by a visionary founder. It is highly unusual for a company in this stage to lose its CEO.

Presumably the CEO was put in charge of the company because he had either great ideas or a plan on how to execute them.

Toby Neugebauer, Fermi’s CEO and Miles Everson, (CFO) have resigned unexpectedly.

We do not have access to any insider information, so we can only speculate as to why they would leave their C-suite positions with the company at such an early stage.

Presumably they would want to see things through if they were excited for the future of the early growth company. Thus, unexpectedly quitting points to something quite negative.

The market seems to have drawn a similar conclusion with the stock down as much as 20% on the day of the announcement.

This leaves Fermi in a precarious spot.

- Asset value is still about a third of market cap even after price declines

- Operating business has been delayed

- Idea value is significantly diminished with the departure of key personnel

It is an idea company that lost its visionary.

Matters are made worse by having a very limited timeframe in which to figure things out.

Hemorrhaging capital as revenues get delayed

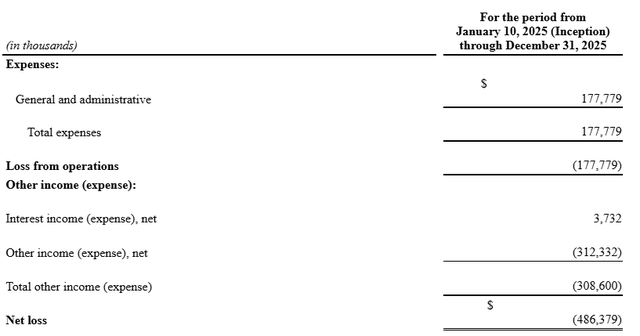

While revenues got delayed, expenses are already ramping up. In 2025 the company had net losses of $486.4 million.

10-K

That is a significant portion of their capital. At this rate of burn, Fermi really needs to get some sort of revenue quickly.

Wrapping up the continued bear thesis

Even at its reduced price, Fermi’s market cap appears significantly larger than the combined value of its assets, business, and ideas. The road ahead looks challenging with expenses putting a clock on how quickly they need to get it together.

Thus, I remain significantly bearish on Fermi.

With that in mind, I want to spend a bit of time addressing the potential bull thesis:

Bull case for Fermi

Data centers are indeed in very high demand.

So far much of the buildout has been able to just be added to the existing electric grid which has reduced the friction to new data center builds.

As time goes on, however, the grid is running out of excess capacity and data centers are having to shift to supplying their own power. Fermi’s mega-campus is a potential solution to this problem as they would connect the various entities to create an all-in-one turn-key solution.

- Land

- Power equipment suppliers

- Connectivity (fiberoptic and power back-up)

- Data centers

The upside to Fermi would be a scenario in which they are able to assemble the full suite while individual players in the space have difficulty navigating the frictions. To the extent Fermi’s mega-campus becomes an increasingly scarce solution, they could charge very high rent.

Why I think the Fermi bull case is unlikely to play out

One of the greatest sources of friction in coordinating all the aspects of building a new data center is having to match a tenant with the power equipment such that everything can be financed.

In my opinion there are 2 lower friction ways to accomplish the buildout of new ground-up data centers.

- Dedicated large cap data center REITs like Equinix (EQIX) or Digital Realty (DLR) who have the enormous balance sheets to fund every aspect in-house such that can just do it autonomously without having to pre-secure tenants.

- The data center customers can self-build. Most of the hyperscale end-users like Google and Microsoft are already building their own.

Equinix is getting expensive, but it is the best in class.

The other friction is the electricity generation side of things. Electric utilities are well positioned to handle this problem. They are experienced in building generation infrastructure and have plans in place to add hundreds of billions of dollars of new plants and transmission lines.

Electric utilities can service future data center needs directly through direct connects or through the grid where new data centers become just part of the now bigger load. The utilities have traded up a bit, but still remain attractively valued given the clear runway of demand growth.

I consider Fermi to be an unnecessary additional middleman. Given the unfavorable valuation and limited visibility on revenues I think it is far more lucrative to just invest in those who have already built a working model.

#Dropping #Fermi #Worth #NASDAQFRMI